Paying off debt was one of the hardest things I’ve ever had to do. The amount was staggering and I felt, at first, like it would never happen.

But I’ve paid off my debt twice now and have sworn to never go back. Because debt freakin’ sucks and I’m sick of being broke. Im sure you are, too.

So you’re faced with a dilemma: how to get started and how to pay off your debt. It’s okay to be a little bit overwhelmed, because that was me as well when I first started my #debtfreejourney. But that’s why I’m here to help. I know how it feels to be in your place. To be crushed by debt. So let me show you how to start, how to get out of debt, and how to build wealth. It’s possible and you CAN do it. So where do we start?

Let’s start off by figuring out something really simple. Which loan do we pay off first – highest interest or smallest debt? Here’s the answer.

Should I pay off my highest interest debt or my debt with the smallest balance first?

You should always pay off your smallest debt first because you want to start off your debt free journey with a quick win that offers immediate progress as well as the inspiration, encouragement, and motivation to keep going.

By crushing that first debt in a short period of time, you’re starting off your debt plan with a HUGE achievement that could potentially fuel the momentum for the rest of your debt free journey! By paying off the smallest debt first, you’re working the “Debt Snowball.”

Now a lot of bloggers will tell you to start with the highest interest rate and work down. If you start with the highest interest rate, you’re working the “Debt Avalanche.” In theory, this should be the smart way to go. It could help you pay off the debt quicker and possibly save you some interest, but this plan has flaws and many people can’t stick to it.

When you’re paying off debt, you have to be able to stay motivated for long periods of time. The debt snowball helps you stay motivated by continually winning over that long period of time. With the debt avalanche, you have to grind it out over a LONG period of time on each debt with a large balance and a large interest rate. This can suck and is primarily why people fail to stay disciplined and continue on their debt free journey.

Interest rate doesn’t matter if you fail to continue paying and stop your mission to pay off your debt. That’s why I say smallest debt first, because you will quickly pay it off and start your debt free journey with an immediate win and the motivation to continue on.

Behavior, math, and motivation

You see, when it comes to paying off debt, it’s 80% percent about behavior. And it’s only 20% percent about math. You obviously need to do the math to figure out all of your debts, exactly how much you owe, exactly how much you make, and exactly how much you can pay on your debt. But all of that is only a small percentage of what you will be doing to actually pay off your debt.

The 90% percent portion is all about behavior because you have to continue paying every month, you have to stay disciplined and motivated to continue paying, you have to keep working hard every day to bring in as much money as possible, and then do ALL OF THAT for 12-18 months or longer. The math is simple. The behavior is tough.

The Debt Snowball vs. The Debt Avalanche

Debt Avalanche

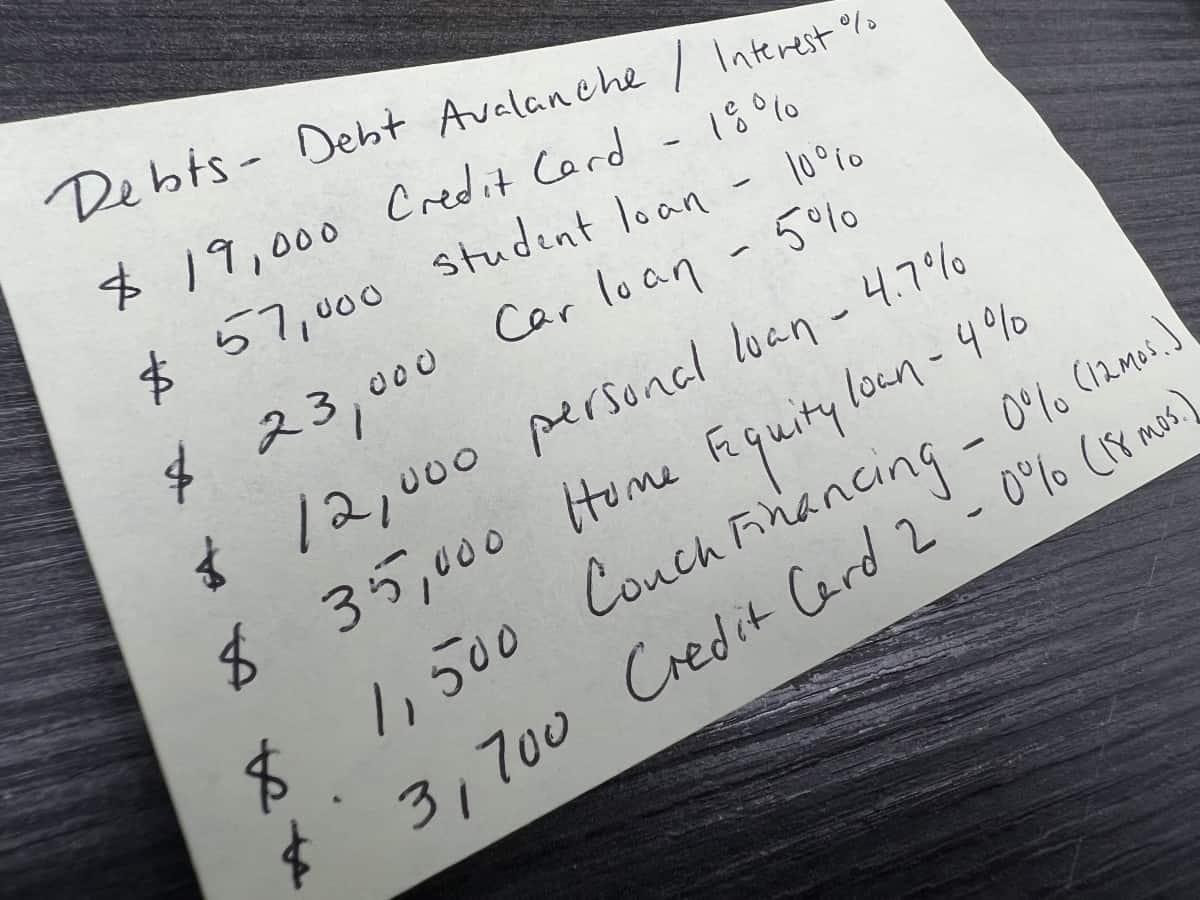

The debt avalanche is a popular financial plan in which you pay off your debts starting with the highest interest rate first. You list your debts from highest interest rate to lowest interest rate and work your way down the list without concern for the balances of each individual loan. Pay minimum payments on all other loans and put the rest of your money toward the highest interest rate loan.

Here’s a good pic of an example set of loans and their subsequent interest rates:

Pros:

- With the avalanche, your overall balance can decrease quicker.

- You also may possibly save on interest fees meaning you may save more money over the course of your debt free journey.

- This could be a good plan if you have a couple of high interest loans that really need to be taken care of to gain traction with your debt.

Cons:

- The highest interest loan is likely to be the debt with the highest balance.

- This plan can be discouraging when little progress is made on a large loan.

- You’re also most likely not getting any quick wins like when you pay a small debt off.

- A lot of people won’t continue this plan because there’s no encouragement or motivation for long periods of times.

- It also doesn’t make sense for low interest rates with limited time frames or terms that change after a period of time (0% percent interest for 12 months, etc, because you will often run out of time).

Debt Snowball

The debt snowball is an extremely popular financial plan in which you pay off your debts starting with the smallest balance first. List your debts from smallest to largest and work your way up without concern for the interest rates on any of the loans. Pay minimums on all other debts and aggressively attack the smallest debt until it’s paid.

Here’s a good pic of an example set of loans and their subsequent balances from smallest to largest:

Cons:

- With the snowball, you might possibly pay more interest over the course of the plan.

- This could extend the length of time in debt or time working the plan.

- The snowball could be tough if you have considerably high interest rates on numerous loans.

Pros:

- You’ll almost always have quick wins to celebrate.

- You can reduce the number of debts you have faster.

- It’s always motivating to check something off quickly.

- People being able to see their debts decrease in a short time can give a motivational boost to pay off debt faster and more aggressively.

- By the time you get to the last, largest debt, you will be on fire! You’ll be so ready to get rid of it that you’ll do everything you can to get it gone.

- The encouragement will keep you on track and this helps a lot of people actually finish this plan.

- Even if you have high interest rates on numerous loans, your snowball will still start growing larger and larger as you stick with the plan.

- Lastly, this plan works with any interest rate and any amount of debt.

Why the debt avalanche just doesn’t work

All in all, the debt avalanche just doesn’t work because people aren’t lifeless robots that compute math, live stagnant lives, and are void of all emotion. The debt avalanche plan only takes into account the math of the equation. It sounds good in theory, but it’s missing out on the motivation behind the debt snowball plan.

People need to feel fulfilled. They need to be encouraged and motivated to continue doing something hard for long periods of time. And the debt avalanche might not offer you any motivation over the course of that timespan. By then, people have already quit the journey and are back to being broke and in debt. That sucks. Don’t be broke and in debt. Use the debt snowball and go win.

Why the debt snowball simply works

The debt snowball gets a lot of negative feedback because, in theory, it might take you a little longer to get through it and it might cost you a couple hundred dollars more in interest. But this is the plan that motivates you to ACTUALLY finish and encourages you every so often with those quick wins. Those wins light you on fire and have you craving to pay off your last debts. That was my experience with it. And when I started paying off debt, the avalanche just didn’t do that for me.

You can choose – but choose wisely

So it’s really up to you. You can choose to do either plan to pay off debt. But I know that you will like the smallest to largest, debt snowball plan better. Give that a try. Because I want you to be able to keep going when the going gets tough. And I don’t want you to fail and quit paying on all of that debt. You can’t let it hang around forever. So get it out of your life as fast as possible! Alright, check out the next section. There are 5 tips to help you destroy your debt fast so that you can start enjoying your money and building wealth!

How to pay off your debt faster – 5 tips for debt success

1. You have to stop Borrowing

If you don’t stop borrowing money, you’ll never EVER get out of debt. That’s the sad truth that way too many people don’t understand. Why? Because debt is easy and people want stuff now, instead of tomorrow.

But if you’re truly serious about getting out of debt, the first thing you have to do is stop the bleeding and quit borrowing money forever. You can’t get out of debt if you keep borrowing. And you can’t stay out of debt if you continue borrowing. Don’t get trapped in the vicious cycle of debt. Stop borrowing money today!

I’d like like to learn more, check out my post, “How to Stop Borrowing Money: 10 Step Guide to a Debt Free Life.”

2. Use a zero-based budget

I’ve used the zero-based budget now for over 10 years and I LOVE it. It has helped me pay off all my debt twice, cash flow tens of thousands of dollars in expenses and life events, and grow our net worth significantly. Now, I attribute a lot of that to hard work and consistent discipline over the years. But we couldn’t have done anything without the help of a zero-based budget.

A zero-based budget simply accounts for every dollar you make and doesn’t allow for any wasteful spending. If you want to spend money, just make sure you can afford it and then put it in the budget. Boom, you’re good to go.

If you’d like to learn more about this kind of budget, check out my posts below:

7 Ways a Zero-Based Budget is the Best Budget for Your Money

37 Ways to Give Yourself a Raise in Your Budget (#27 is Crazy!)

3. Decrease your expenses

There’s a pretty simple formula for finding more money in your budget: decreasing your expenses + increasing your income = more money to crush debt. Decreasing your expenses is probably the easiest, though, because you’re already spending money. Now all you have to do is find ways to spend less (and there’s a thousand different hacks to cut down your spending).

If you want to get a good handle on your finances, learn how to cut expenses and live off of that set amount.

4. Increase your income

The second part of that equation is to increase your income. Because you can only decrease your expenses so much. You can cut out everything and be an extreme cheapskate but you’re still going to have some living expenses.

On the other hand, income can be almost unlimited. You can always increase your income and many people make A LOT of money per year. Do whatever you can to increase your income so that you can destroy all of your debt.

5. The no-spend challenge

This challenge is awesome. The no-spend challenge is exactly what it sounds like: a challenge to not spend any money over a selected period of time (except for required bills and expenses). This is a very simple challenge to try by the day but it is also tough to do this over a longer period of time. I love doing this challenge on a monthly basis. It’s perfect for helping save money during a really tight month!

Finally

If you’re still not convinced that you need to start out by paying off your smallest debt, that’s okay. I’m not here to tell you that you’re wrong or that I’m right. I’m just telling you what worked for my family and what I believe makes the most sense. Because paying off debt is hard enough as it is. You need some wins and encouragement along the way. And that starts with the smallest debt and the debt snowball. I paid off my debt. I know you can, too!

A couple of posts to help you save and pay off debt

20 Reasons Why Debt is Bad: The 10,000+ Word Complete Guide!

47 Creative Ways to Pay Off Debt [2022 Edition]

17 Personal Finance Tips to Beat Inflation: The 2022 Guide

Freepik attribution

<a href=’https://www.freepik.com/vectors/minimalist-background’>Minimalist background vector created by freepik – www.freepik.com</a>

Vecteezy attribution

<a href=”https://www.vecteezy.com/free-vector/orange-brush-stroke”>Orange Brush Stroke Vectors by Vecteezy</a>