Welcome to DollarDollarNOW! Thank you so much for checking out my site and I hope you find exactly what you’re looking for! If you would like to see the page all about DollarDollarNOW, check that out here.

This page will highlight me and my wife’s financial journey from the time we were 18 until now, over 12 years later. This page highlights all of the ups, downs, and everything in between. The road has been tough and long, but we’ve come through and are looking forward to becoming millionaires over the next 10 years.

First things first – I’m Red.

I’m a dedicated debt free advocate and personal finance expert. I’ve studied personal finance for over 10 years and have grown our net worth from -$30,000 to almost $300,000 as of 02/28/2022 at 30 years old.

I love personal finance and helping others get out of debt.

In the picture below, you’ll see me, my wife Savannah, and our son Declan.

We love our little family and we’re determined to change our family tree and leave a financial legacy behind us.

Here are our FINANCIAL PRINCIPLES:

We don’t borrow money (for anything EVER).

We live below our means.

We use a detailed budget every month.

We have financial goals.

We work our asses off to make more income.

We’re not perfect. But we practice intentionality with our money and we’ve done our best to stay consistent.

My Baby Steps Journey (before we got married)

From 18-22, I borrowed a total of $30,000 dollars for school loans and other miscellaneous stuff on my credit card.

In 2013, I started listening to this interesting money show, with this weird Hillybilly named Dave Ramsey, who spoke about the fact that you can pay your debt off and live “debt free.” Hmm…at first, I was like, “no way, debt is normal, or so I’ve been told. Everyone has loans and car payments.”

But gradually, it all made sense. You pay down your debt anyway over time, right? So why not speed up the process and become debt free as fast as possible.

Now I wish I would’ve been gazelle intense (super hardcore about paying off debt FAST), but I wasn’t. I did really well, and I had a goal of paying off all my debt, but it still took me about 40 months. I started making only $9/hr or about $1,200 per month. So it wasn’t easy in the beginning. But with support from my girlfriend-turned-fiance-now-wife, I started paying as much as I could every month toward paying my debt off. Not long before we got married, I paid off my debt and I was debt free ($30,000 paid in about 40 months). It took me from about 2013-2016 to do this. Sav was lucky not to have any school debt and only a small car loan coming into the marriage.

In 2016, We focused on paying cash for our wedding. In about 14 months, we cash flowed our $10,000 wedding. With the help of our wedding present money, and 1 plane ticket being purchased for us, we paid all cash for our dream Italy honeymoon trip and cruise.

Not long after the wedding, Savannah had a new goal: getting her Master’s Degree. We knew it was going to take 3 years and cost $12,000 dollars. But she wanted this to advance her future career. So she did it and we cash flowed $4,000 per year for 3 years from 2017-2019. Masters Degree paid for. It helped that there were some tax credits giving us back a small portion of what we paid each year.

Sav got pregnant in Fall of 2018 and so we knew that she would finish her Masters Degree in Spring of 2019. We also knew that we would have to cash flow the baby. I definitely wasn’t owing money on my newborn baby. So we paid a total of around $6,000 dollars and officially owned our newborn baby when he got here!

Then, in October of 2019, we ended up making a pretty bad financial mistake. We bought a $30,000 dollar Toyota Highlander. It was a fantastic family purchase but it really ate up a lot of our income every month. Almost $400 per month. On top of all the added baby expenses, that made us live paycheck to paycheck. We did put down about $5,500 onto the Highlander but we still owed around $25k for it.

We kept paying our minimums from October to March and I finally got fed up…if we had done so good with money, why were we living paycheck to paycheck again?! We had Sav’s Dodge Dart, our Toyota Highlander, New phones, and we were overspending with no budget to keep it in check.

That was my breaking point. I’m done. I’m never borrowing money again. I’m paying off our stupid debt and actually following the Ramsey baby steps plan that helped me so much up to this point. We had $29,166.30 in debt and I was done with it.

Our Baby Steps Journey

It took me a really long time to get Sav on board with the Ramsey Baby Steps…about 7 years. But we finally got on the same page.

We started baby step 1 in March of 2020. Baby step 1 completed in March of 2020.

We started baby step 2 in March of 2020.

I used our $3,500 tax refund to jump start the whole process. I thought we only had the two cars as debt so the Dart was paid off. That’s $200 extra per month. We paid the phones off once I realized that it was debt and that it was stupid to be financing a phone. That was around $2,000 total for Sav’s phone and mine. That was another $100 dollars extra per month freed up in the budget.

All of that extra money started adding up and got put into our debt snowball! The debt snowball is simple. Imagine a snowball rolling down a hill. As it keeps going, it picks up more and more snow and gets bigger and bigger. That same thing applies to your debt snowball. When you pay something off or find a way to save some money, you add that money into a snowball of cash. The $200 from my car started it. I paid off phones and added in another $100 up to a total of $300. We cut a few expenses and worked our way up to $500 per month extra. As you pay more things off, you keep adding to that total amount and the amount you can put on the next debt gets bigger and bigger.

On top of all that, Sav and I have been able to add a little bit of income to that total and I’ve added any raises into that as well. You have to cut as many expenses as you can AND you have to work your ass off to make more money. Thats how you pay stuff off and do better with money.

Oh, and don’t forget the budget. You HAVE TO have a budget every month and you need to track every expense down to the nearest dollar. We track expenses down to the cent. Sav and I want to know exactly where every penny is going.

Check out our debt snowball below ⬇️. You can see that we started a little out of order with the Dave Ramsey baby steps, but we decided a few months in to fully commit and we used 4,000 of the emergency fund to really speed up our debt payoff.

To date, Sav and I are debt free and everything is paid off but our home. During the first part our #debtfreejourney, Savannah and I paid off a total of $29,166.30 and completed baby step 2 in February of 2021.

We started baby step 3 in February of 2021. We were looking to get to $10,000 dollars into our emergency fund or 3 months of expenses. Baby step 3 was completed in May of 2021.

We are now on to baby step 4, 5, and 6. We are investing 15% of our incomes, putting about $100 per month into our son’s 529 college savings plan (with a goal of $200 per month in the near future), and crushing extra payments on our home.

Our Overall Stats

To date, we’ve paid: $59,166.30 in debt

We’ve also cashflowed: around $30,000 in events (wedding, honeymoon, masters degree, and baby)

Total of $89,166.30 paid

Total of $10,000 in emergency fund

Our New Goal

Now that we’re debt free, we are shooting for a huge new goal. We recently refinanced our home from a 30 year mortgage down to a 15 year mortgage due to the outrageously low interest rates during the Covid Pandemic.

Our new goal is to pay off that 15 year mortgage in 5 years from the date we started making extra payments. From March to May, we were finishing up the emergency fund. And from May to August, we decided to buy some stuff that was wanted and needed, get some much needed repairs on the house, and go on vacation.

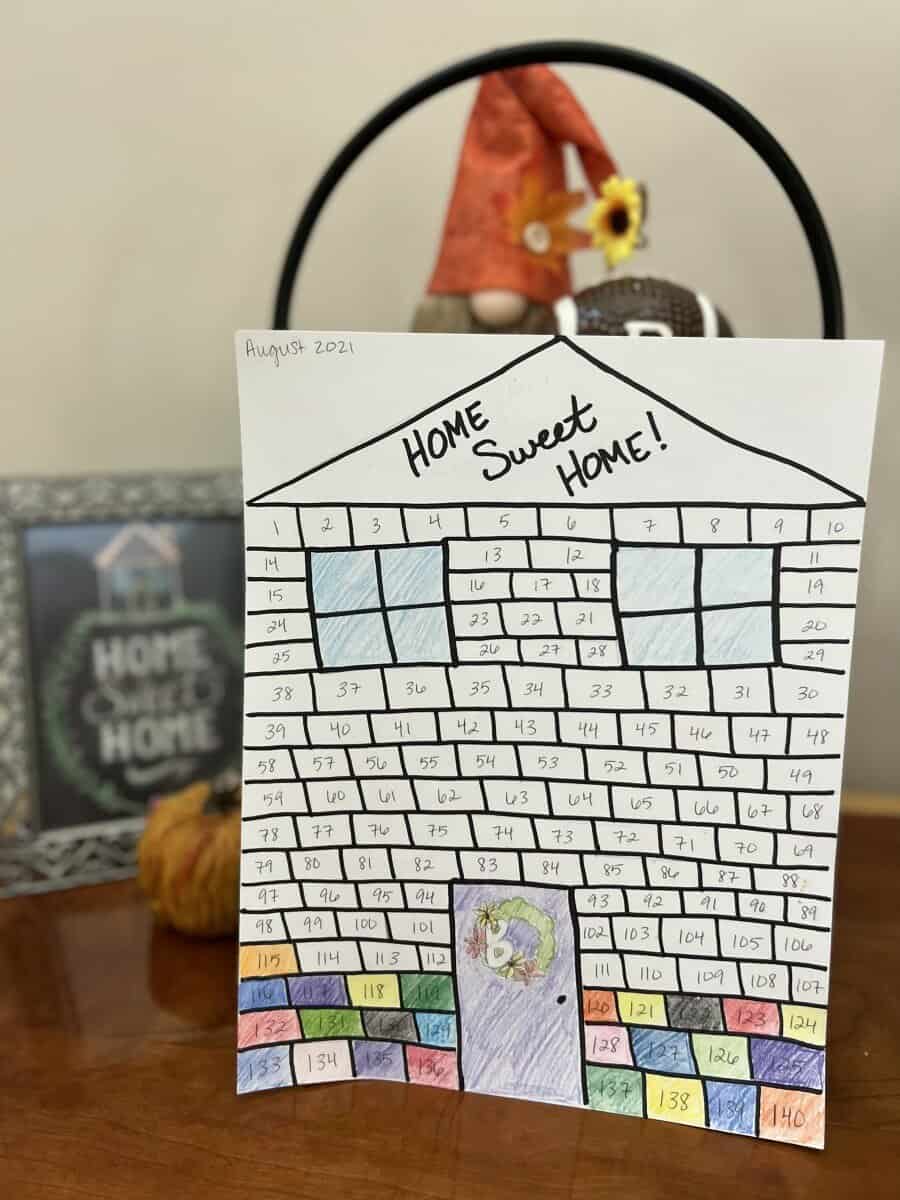

We started talking about the house in about June and thought it would be pretty crazy to have it paid off in 5 years. But that would require a DOUBLE mortgage payment. An extra $1200 dollars every month for 5 years. We decided to give it a shot and started making the extra payment in August of 2021. $140,000 dollars to go.

Check out our mortgage payoff form below ⬇️. We color off a block every time we get below the number listed. So once we get below 126,000.00, we will color off the “126” block. We decided to start from the bottom and color up so that we would be starting with the foundation and building up our home/building our equity.

As of today, September 17th, 2022, our mortgage sits at $114,582.60 and should be paid off by around August of 2026.

As of today, February 28th, 2022, our mortgage sits at $126,805.23 and should be paid off by around August of 2026.

So What’s Next for Us?

I like to think a fully paid-for house at 35 years old and millionaire status at 40. Savannah and I also want to help our son go to college debt free. Hefty goals, but hey, why not?

If you’d like to reach out to us for any reason, send an email to dollardollarnowofficial@gmail.com